Ever wondered how your online purchases actually go through? It’s not just magic! There’s a whole system working behind the scenes, and a payment gateway flowchart helps us see it clearly. Think of it like a digital messenger carrying your payment info safely from your computer to the bank and back. It’s a pretty neat process, and understanding it can make you feel more in control when you’re shopping online. Let’s break down how this whole payment gateway flowchart works, step by step.

Key Takeaways

- A payment gateway is like a digital checkpoint that securely moves payment information between customers, merchants, and banks.

- The process starts when a customer pays, their data is encrypted, and sent for authorization.

- Banks verify the customer’s account, then send back an approval or denial.

- This entire authorization cycle happens very quickly, usually in just a few seconds.

- After approval, the transaction is settled, and funds eventually reach the merchant’s account.

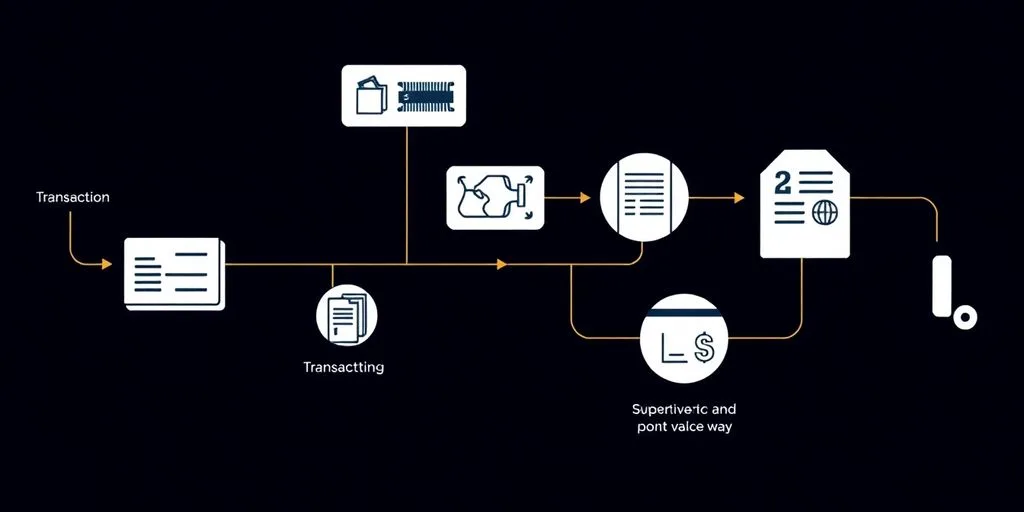

Understanding The Payment Gateway Flowchart

Think of a payment gateway as the digital equivalent of a cashier in a physical store. It’s the technology that makes sure your customers can pay you securely and efficiently, whether they’re buying something online or in person. It’s the crucial link that connects your business to the financial networks needed to process payments. Without it, accepting card payments would be a whole lot harder, if not impossible.

What is a Payment Gateway?

A payment gateway is essentially a service that authorizes and transmits payment information from a customer to the merchant’s bank. It captures payment details, like credit card numbers or bank account information, and sends them securely for processing. For online businesses, this often means integrating a gateway into their website or app. For physical stores, it might be the terminal at the checkout counter. It’s the first step in getting your money from the customer to your business.

Role of a Payment Gateway

The main job of a payment gateway is to act as a secure intermediary. It takes sensitive payment data, encrypts it, and sends it through the payment processing network. It also receives the approval or denial message and relays it back to the customer and merchant. Beyond just moving data, gateways help streamline cash flow and can even help with fraud detection, making the whole payment process smoother and safer for everyone involved. They are pretty important for any business that wants to accept payments beyond cash.

Payment Gateway vs. Payment Processor

People often mix these two up, but they do different things. A payment gateway is like the secure tunnel for your payment data – it captures and encrypts the info. A payment processor, on the other hand, is the engine that actually moves the money. It handles the communication between the banks and the card networks. You need both for a transaction to happen, but they have distinct roles in the process. Think of the gateway as the messenger and the processor as the delivery service.

The Step-by-Step Payment Gateway Process

So, you’ve got your online store humming, customers are adding items to their carts, and then… the checkout. This is where the magic, or sometimes the frustration, happens. Understanding the step-by-step process of how a payment gateway handles a transaction can really demystify the whole thing. It’s not just a button that says ‘Pay Now’; there’s a whole chain of events happening behind the scenes, usually in just a few seconds.

Customer Initiates Transaction

It all starts with the customer. After picking out their goodies, they proceed to checkout. This is where they’ll enter their payment details, like credit card numbers, expiry dates, and CVV codes. Think of this as the customer handing over their payment information to the merchant’s system.

Data Encryption and Transmission

Once the customer hits ‘submit’, the data they just entered needs to be protected. The merchant’s website or app uses something called SSL encryption to scramble this sensitive information. This encrypted data then travels from the customer’s browser or app to the merchant’s web server. The payment gateway takes over here, often handling the sensitive data so the merchant doesn’t have to store it directly, which helps with PCI DSS compliance.

Transaction Authorization

This is the core of the process. The payment gateway sends the transaction details to a payment processor. This processor then communicates with the card networks (like Visa or Mastercard) and eventually reaches the customer’s issuing bank. The issuing bank checks if the customer has enough funds and if the card details are valid. It’s like a quick check to see if the payment is good to go.

This entire authorization phase, from the customer clicking ‘pay’ to getting a ‘yes’ or ‘no’ response, typically happens in under three seconds. It’s a rapid-fire exchange of information across multiple financial entities.

Here’s a simplified look at the initial steps:

- Customer Enters Details: Payment information is provided at checkout.

- Data Secured: Information is encrypted using SSL.

- Gateway Receives: The payment gateway securely collects the encrypted data.

- Processor Forwarded: Data is sent to the payment processor.

- Network Communication: Processor communicates with card networks and issuing banks.

Navigating The Authorization and Settlement Stages

Once a transaction gets the green light from the issuing bank, it moves into the authorization and settlement phases. This is where the actual money starts to move, and it involves a few more steps to make sure everything is accounted for.

Issuing Bank Verification

This is where the customer’s bank, the one that issued their card, takes a close look. They check if the customer has enough funds or credit available. They also look at things like account status and any potential fraud flags. This verification is key to approving or denying the transaction. It’s a quick check, but it’s super important for preventing losses.

Authorization Response

After the issuing bank makes its decision, it sends a response back. This response travels through the card network and the acquiring bank, eventually reaching the payment processor and then the payment gateway. The gateway then tells the merchant whether the transaction was approved or declined. If it’s approved, the sale goes through. If not, the customer might need to try a different payment method.

Transaction Settlement

Settlement is the actual transfer of funds. At the end of the day, the merchant sends all the approved transactions in a batch to their acquiring bank. This batch is then sent to the card networks, which communicate with the issuing banks. The issuing banks then send the money to the acquiring banks, and finally, the acquiring banks deposit the funds into the merchant’s account. This whole process can take a day or two to complete, but it’s how the money officially changes hands. It’s a bit like clearing a check, but much faster and more automated. This is how payment processors facilitate the transfer of funds.

Key Components of Payment Processing

When you buy something online or in a store, a bunch of different players are involved behind the scenes to make sure your money gets from your bank account to the seller’s. It’s not just magic, though it can feel like it sometimes. Let’s break down who’s who in this whole payment process.

The Customer and Merchant

First off, you’ve got the customer, that’s you, the person actually making the purchase. Then there’s the merchant, the business or individual selling the goods or services. These two are the starting and ending points of any transaction. Without a customer wanting to buy and a merchant wanting to sell, there’s no payment to process.

Payment Method and POS System

Next up is how you actually pay. This is the payment method – think credit cards, debit cards, maybe even a digital wallet like Apple Pay or Google Pay. Whatever you use, it needs to be accepted by the merchant. The place where you make this payment is the POS system, or Point of Sale system. This could be the card reader at a physical store, the checkout page on a website, or even an app on a phone. It’s the terminal that captures your payment details.

Card Networks and Financial Institutions

After your payment info is captured, it goes through a few more important channels. The card networks, like Visa, Mastercard, or American Express, are the big companies that set the rules for how transactions happen using their cards. They act like a highway system for payment data. Then you have the banks. The issuing bank is the bank that gave you your card. They check if you have enough money and approve or deny the transaction. The acquiring bank is the merchant’s bank; it receives the money on behalf of the merchant. It’s a whole team effort to get that money moved correctly. Understanding these different parts helps explain why sometimes a payment might take a moment or why certain cards work at one place but not another. It’s all about how these different financial institutions and networks communicate to complete your purchase. It’s pretty wild when you think about how many steps are involved just to buy a coffee. The whole process needs to be secure, too, which is why things like PCI DSS compliance are so important for businesses handling your card information. It’s all about making sure your financial data is protected at every stage, from the moment you tap your card to when the money actually lands in the merchant’s account. This structured approach helps maintain financial control and prevent errors in the accounts payable process AP process.

The entire payment ecosystem relies on these components working together smoothly. Each part has a specific job, from capturing your card details to verifying funds and moving money between banks. When one piece falters, the whole transaction can be affected, which is why reliability and security are so important for everyone involved.

Ensuring Security in the Payment Gateway Flowchart

Keeping customer data safe is a big deal when processing payments. It’s not just about making sure the money moves correctly; it’s also about protecting all the sensitive information that gets shared along the way. Think about credit card numbers, expiry dates, and even personal addresses. If that stuff falls into the wrong hands, it can cause a lot of trouble for everyone involved.

Data Encryption Standards

One of the first lines of defense is data encryption. This is basically scrambling your data so that only authorized parties can read it. When you use a payment gateway, it typically uses something called SSL (Secure Sockets Layer) or its successor, TLS (Transport Layer Security). These protocols create a secure tunnel between the customer’s browser and the merchant’s server, and then between the server and the payment gateway itself. This means that even if someone managed to intercept the data, it would just look like gibberish to them. It’s like sending a secret code instead of plain English.

PCI DSS Compliance

Then there’s the Payment Card Industry Data Security Standard, or PCI DSS. This is a set of rules that all businesses that handle credit card information have to follow. It covers everything from how you store data to how you transmit it and who has access to it. Getting PCI DSS compliant can seem like a lot, but it’s really important for building trust with your customers. It shows you’re serious about protecting their financial details. Many payment gateways handle a lot of the heavy lifting for PCI compliance, which is a big help for merchants.

Tokenization for Secure Storage

Another clever security trick is tokenization. Instead of storing actual credit card numbers, businesses can use tokens. A token is like a stand-in, a unique identifier that represents the cardholder’s data. When a customer makes a purchase, their card details are sent to the payment gateway, which then replaces the actual card number with a token. This token can then be used for future transactions without needing to handle the sensitive card information directly. It significantly reduces the risk if a system is breached because the attackers would only get tokens, not the real card numbers. This is a really smart way to handle customer payment data.

Protecting financial information isn’t just a technical requirement; it’s a core part of maintaining customer trust and the overall integrity of the payment process. Businesses that prioritize security build stronger relationships with their customers and reduce their own risk exposure.

Types of Payment Gateways

So, you’ve got your online store humming along, and now you need to figure out how people can actually pay you. That’s where payment gateways come in, but not all of them are built the same. Think of it like choosing between a simple cash register and a fancy, integrated system for your shop. The type you pick can really change how customers interact with your checkout process and how much control you have over things.

On-Site Payment Gateways

These are the ones where everything happens right on your own website. Your customers never leave your digital doorstep to pay. This gives you a lot of control over the look and feel of the checkout page, which can be great for branding and customer experience. However, it also means you’re responsible for handling all the sensitive payment data yourself. This usually means you need to be extra careful about security and compliance, like PCI DSS. It’s often favored by larger businesses that have the resources to manage this.

Off-Site Payment Gateways

With off-site gateways, when it’s time to pay, your customer gets sent to a different website – usually the payment provider’s site – to finish the transaction. It’s like having a separate payment booth at a market. The upside here is that the payment provider handles all the security and data storage, which can be a big relief. It simplifies things for you, the merchant. The downside? You lose a bit of control over the customer’s final checkout experience, and some customers might get a little wary if they’re suddenly on a different site. It’s a common choice for small to medium businesses that want a simpler setup. A good example of this is using a third-party payment page.

Hybrid Payment Gateways

These try to offer the best of both worlds. A hybrid gateway might let the customer start the checkout on your site, but then it can either keep them on your site using secure frames or pop-ups, or it might redirect them to the provider’s page if that’s what the customer prefers or if it’s deemed more secure for a particular transaction. It’s a flexible approach that aims to balance user experience with security and control. You get some of the branding control of on-site, with some of the security benefits of off-site, depending on how it’s configured.

Choosing the right type of payment gateway really depends on your business size, your technical capabilities, and how much you want to manage the checkout process yourself. It’s not a one-size-fits-all situation.

Wrapping It Up

So, that’s the basic rundown of how a payment gateway actually works. It might seem like a lot of steps, and honestly, it is, but it all happens super fast. From the moment you hit ‘buy’ to getting that ‘order confirmed’ message, there are several systems talking to each other to make sure your money gets where it needs to go, safely. Understanding this flow helps you see why these systems are so important for online shopping and why businesses rely on them to keep things running smoothly. It’s a pretty neat piece of tech when you think about it.

Frequently Asked Questions

What exactly is a payment gateway?

Think of a payment gateway as a digital cashier for online stores. It’s the technology that safely takes your payment details, like your credit card number, and sends them to the bank to check if you have enough money. It’s like a secure tunnel for your payment information.

Why are payment gateways so important for online shopping?

A payment gateway is super important because it makes sure your money gets from your bank to the store’s bank safely and quickly. It’s like a messenger that carries your payment information and makes sure everything is okay before the money moves.

What’s the difference between a payment gateway and a payment processor?

While they work together, a payment gateway is like the front desk that collects your payment info. A payment processor is more like the back-office worker that actually moves the money between banks and makes sure the transaction goes through. The gateway gets the info, and the processor handles the money.

How does a payment gateway handle my card information?

When you pay, the gateway first scrambles your card details so no one can read them. Then, it sends this scrambled info to your bank to see if you can pay. Your bank sends back a message saying ‘yes’ or ‘no.’ The gateway then tells the store if the payment worked.

How do payment gateways keep my information safe?

Security is a big deal! Payment gateways use special codes (encryption) to protect your information, like a secret language. They also follow strict rules, like PCI DSS, to keep your data safe. Sometimes, they even swap your real card number for a secret code (tokenization) to keep it extra secure.

Are there different kinds of payment gateways?

There are a few main types. Some gateways let you pay right on the store’s website. Others send you to a different, secure page to pay. And some let you choose between staying on the site or going to a separate page. It all depends on how the online store is set up.